Program: Start Your Personal Tax (T1) Preparation Business

Module-3- Understanding Various T-Slips

Lesson-M-3-L-1-T4-Employment Income

This Lesson summarize the essential rules every payroll preparer, bookkeeper, or new firm owner must understand when preparing T4 slips for employees.

1. What Is a T4 Slip?

A T4 slip reports all remuneration an employer paid to an employee in a calendar year. Employees use this slip to complete their personal tax returns.

T4s must be issued for:

-Employment income

-Commissions

-Taxable allowances and benefits

-Fishing income

-Any other taxable remuneration

You must issue a T4 if:

-You deducted CPP/QPP, EI, PPIP, or income tax

-OR total remuneration exceeded $500 (unless on the exception list)

2. Identification Section

Year

Enter the calendar year in which the employee was paid.

Employer Name

Use your legal name and operating name (if different), plus address.

Employee Name & Address

Use CAPITAL LETTERS

Last name → First name → Initials

No titles (Mr., Mrs., Director)

Include full home address, province/territory, postal code, and country

3. Box 10 – Province of Employment (POE)

POE is based on where the employee reports for work, not where the employer is located.

Examples:

Employee works remotely in BC → POE = BC

Employee works on an offshore oil rig → POE = ZZ

Employee works outside Canada (not US) → POE = ZZ

If an employee worked in more than one province, issue separate T4 slips.

4. Box 12 – Social Insurance Number (SIN)

Use the SIN provided by the employee

If no SIN → enter 000000000

If employee had a temporary SIN starting with 9 but later received a permanent SIN → use the permanent SIN

Do not issue two T4s

5. Box 28 – Exempt (CPP/QPP, EI, PPIP)

Check the exemption box ONLY if:

-You did not have to deduct CPP/QPP, EI, or PPIP for the entire reporting period

-OR you used an employment code in Box 29

Do not check the box if you reported amounts in the corresponding CPP/EI/PPIP boxes.

6. Box 29 – Employment Codes

Use these only when applicable:

Code Description

11 Placement/employment agency workers

12 Self‑employed taxi or passenger‑vehicle drivers

13 Self‑employed barbers/hairdressers

14 Prescribed salary deferral arrangement withdrawals

15 Seasonal Agricultural Workers Program

16 Detached employee under a social security agreement

17 Self‑employed fishers

If none apply → leave blank.

7. Box 45 – Employer‑Offered Dental Benefits

Mandatory for 2023 onward.

Codes:

1-Not eligible for any dental coverage

2-Employee only

3-Employee, spouse, and dependent children

4-Employee and spouse

5-Employee and dependent children

Important notes:

-Report eligibility, not whether the employee used or declined coverage

-If employee left before Dec 31 → use code 1

-HSAs count only if they cover dental services

-Union‑provided benefits are reported only if the employer is involved in providing them

8. Box 14 – Employment Income

Report total employment income before deductions.

Includes:

Salary, wages, commissions

Bonuses, vacation pay

Taxable benefits

Controlled tips

Wage‑loss replacement benefits

Non‑qualifying SUBP top‑ups

EBP payments

Board and lodging (code 30)

Travel benefits (code 32/33)

Automobile benefits (code 34)

Low‑interest loan benefits (code 36)

Security option benefits (code 38 or 90)

Do not include:

-Retiring allowances (codes 66/67/69)

-Tax‑exempt First Nations income

-Income reported under employment codes 11–17

-Qualifying SUBP payments (reported on T4A)

9. CPP/QPP and CPP2/QPP2 Contributions

Box 16 – CPP Contributions

Use when POE is not in Quebec.

Box 16A – CPP2 Contributions

Use for second‑tier CPP contributions (2024 onward).

Box 17 – QPP Contributions

Use when POE is Quebec.

Box 17A – QPP2 Contributions

Use for second‑tier QPP contributions (2024 onward).

Key rules:

-If you report CPP/QPP contributions, you must also report pensionable earnings in Box 26

-Over‑deductions must be reported unless reimbursed

-Under‑deductions are corrected separately (not on the T4)

10. Box 18, 22, 24,26

Box 18 – EI Premiums

Report EI premiums deducted.

If you report EI premiums, you must also report insurable earnings in Box 24.

Box 22 – Income Tax Deducted

Report the total federal and provincial tax withheld.

Box 24 – EI Insurable Earnings

Usually equals employment income unless:

-Certain benefits are excluded

-Employee is non‑arm’s‑length

-Employee worked in Quebec (different EI rules)

Box 26 – CPP/QPP Pensionable Earnings

Often equals Box 14, but can differ in cases such as:

-Non‑cash benefits

-Quebec‑specific rules

-CPP2/QPP2 thresholds

10. Box 18, 22, 24,26

Box 18 – EI Premiums

Report EI premiums deducted.

If you report EI premiums, you must also report insurable earnings in Box 24.

Box 22 – Income Tax Deducted

Report the total federal and provincial tax withheld.

Box 24 – EI Insurable Earnings

Usually equals employment income unless:

-Certain benefits are excluded

-Employee is non‑arm’s‑length

-Employee worked in Quebec (different EI rules)

Box 26 – CPP/QPP Pensionable Earnings

Often equals Box 14, but can differ in cases such as:

-Non‑cash benefits

-Quebec‑specific rules

-CPP2/QPP2 thresholds

11. Special Situations to Know

Multiple provinces → separate T4s

Detached employees → use code 16

Overpayments → report only if not repaid or repaid without performing duties

Tax‑exempt First Nations income → use code 71 or 88

Emergency volunteers → taxable portion in Box 14; exempt portion (up to $1,000) in code 87 Board/lodging at special work sites → use code 31 (tax‑exempt)

12. Common Errors to Avoid

Incorrect POE (Box 10)

Missing dental benefit code (Box 45)

Reporting CPP/QPP without pensionable earnings

Incorrect EI insurable earnings

Reporting retiring allowances in Box 14

Using Box 28 incorrectly

Not issuing multiple T4s for multiple provinces

13. Key Takeaways

The T4 slip is a legal reporting document — accuracy matters

Always match deductions with corresponding insurable/pensionable earnings

Understand special situations to avoid CRA reassessments

Consistency across all slips for the same employee is essential

Program: Start Your Personal Tax (T1) Preparation Business

Module-3- Understanding Various T-Slips

Lesson-M-3-L-2-T4A-Pension and Other Income

These lessons summarize the essential rules that every bookkeeper, payroll preparer, and firm owner must understand when preparing T4A slips for contractors, pension recipients, students, retirees, and other recipients of non-employment income.

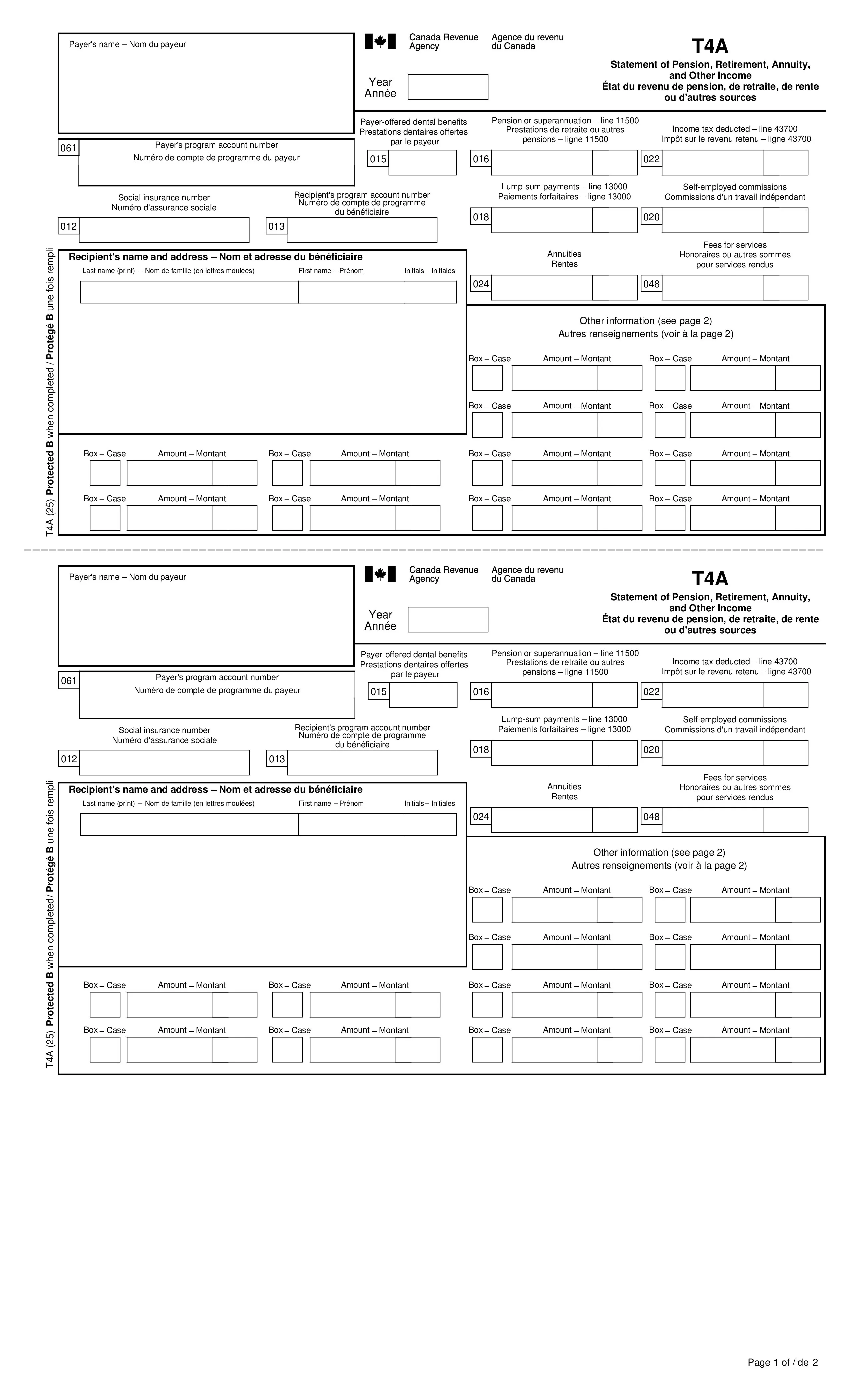

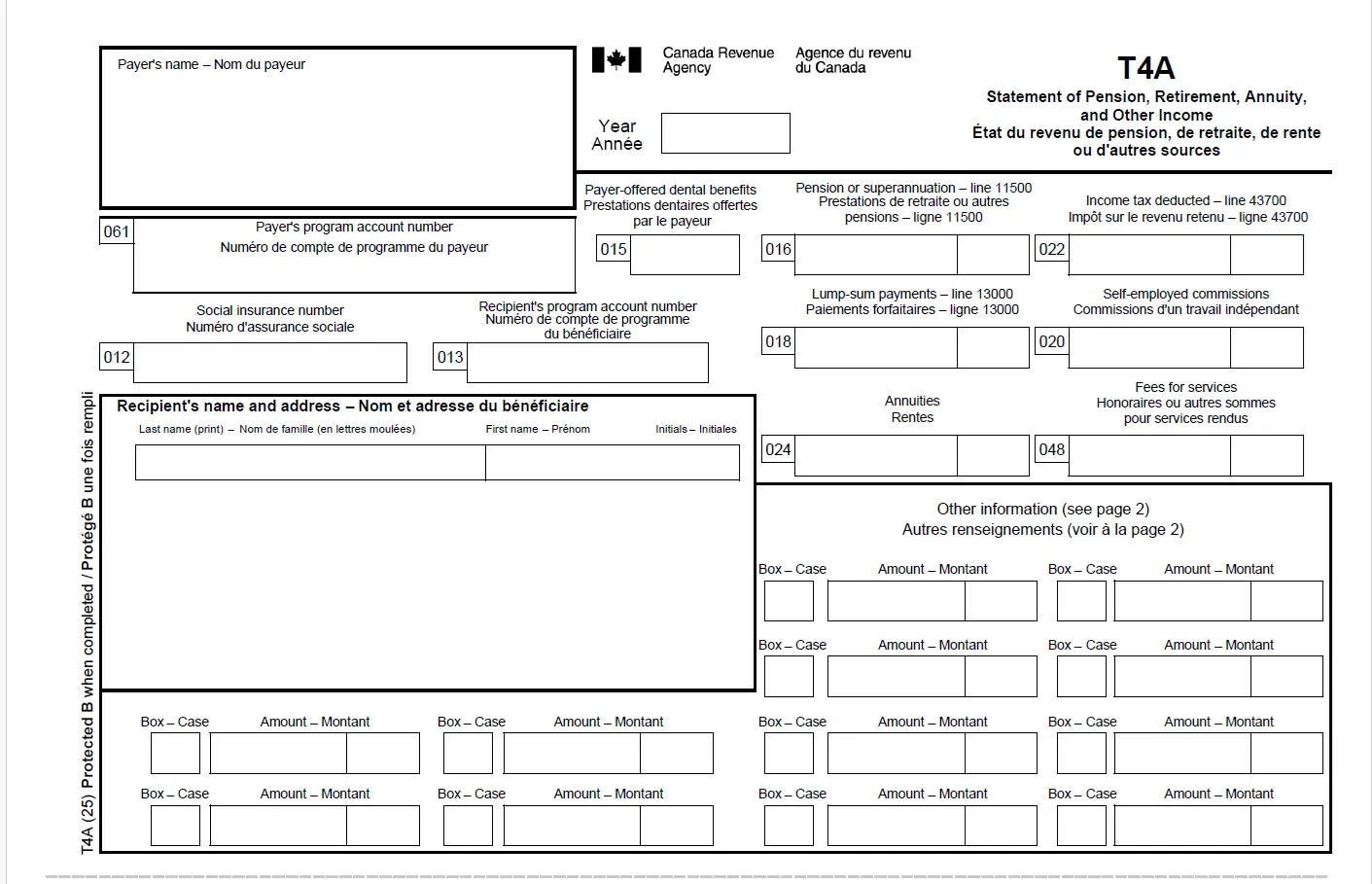

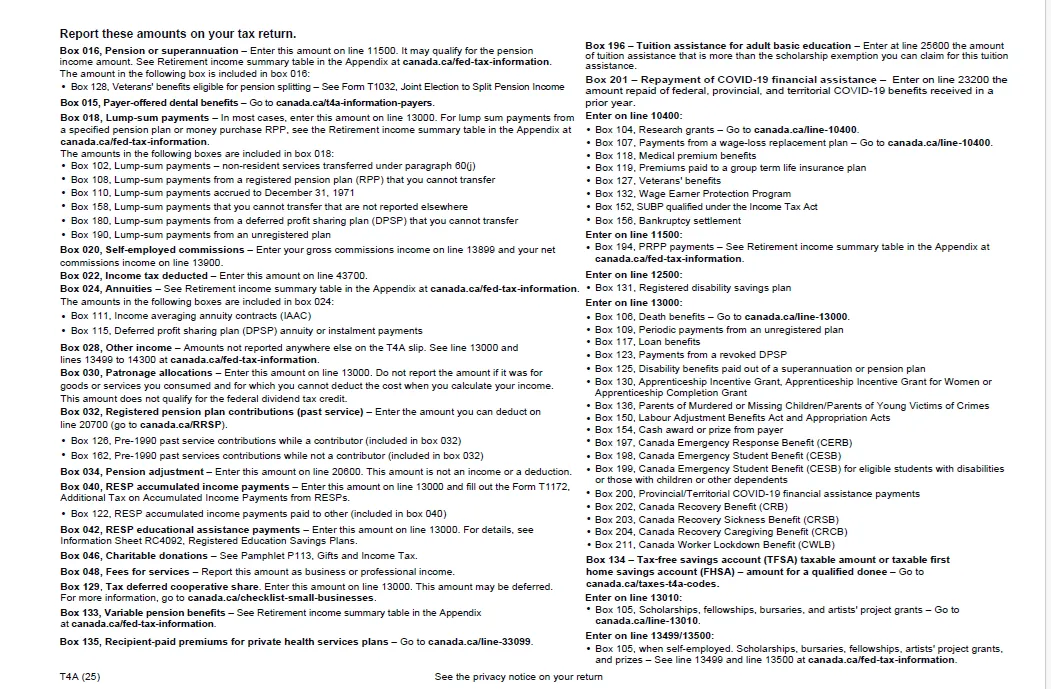

1. What Is a T4A Slip?

A T4A slip reports various types of income that are not employment income. It is used for payments such as:

-Self‑employed commissions

-Fees for services

-Pension or superannuation

-Lump‑sum payments

-RESP payments

-Scholarships, bursaries, and grants

-Certain benefits and allowances

Employees receive T4s.

Contractors, retirees, students, and other recipients may receive T4As.

2. When Must You Issue a T4A?

You must issue a T4A if:

You deducted income tax from any payment

OR total payments exceeded $500 (unless on the exceptions list)

Payers include:

Employers

Trustees

Estate executors/liquidators

Administrators

Corporate directors

Pension plan administrators

3. Identification Section

Year

Enter the calendar year the payment was made.

Payer Name

Use your legal name and operating name (if different).

Recipient Name & Address

CAPITAL LETTERS Last name → First name → Initials

No titles (Mr., Mrs., Director)

Full home address, including province, postal code, and country

Do not put recipient numbers in the address area

4. Box 012 – Social Insurance Number (SIN)

-Enter the SIN provided

-If no SIN → enter 000000000

-If a temporary SIN (starts with 9) is replaced by a permanent SIN → use the permanent SIN

-Do not issue two slips

-If the recipient is a business, do not use a SIN → use Box 013

5. Box 013 – Recipient’s Program Account Number

Use this when the recipient is:

-A sole proprietor

-A partnership

-A corporation

Enter their business number (e.g., 123456789RT0001).

6. Box 015 – Payer‑Offered Dental Benefits

Mandatory only when Box 016 (pension/superannuation) is filled.

Codes:

1 — Not eligible

2 — Recipient only

3 — Recipient, spouse, and children

4 — Recipient and spouse

5 — Recipient and children

Important notes:

-Report eligibility, not usage

-HSAs count if they cover dental services

-Union‑provided benefits are reported only if the employer/pension plan is involved

-Code 1 is optional for 2023–2024 under administrative relief

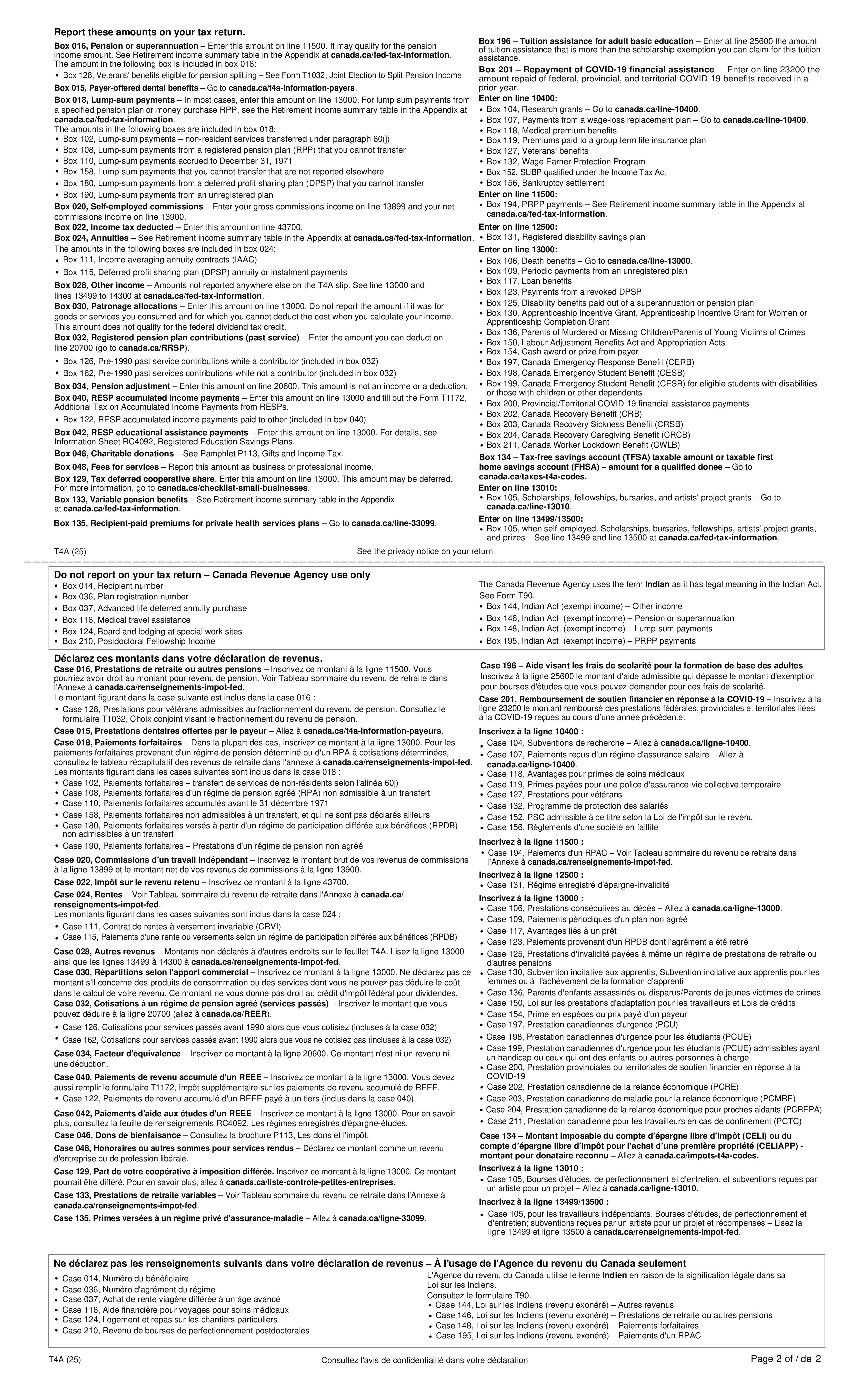

7. Box 016 – Pension or Superannuation

Report:

-Taxable annuity payments from RPPs

-Disability benefits are paid as a life annuity

-Veterans’ benefits are eligible for pension splitting

-Periodic payments from unregistered pension plans (in specific cases)

Do not report:

-Non‑annuity disability benefits (use code 125)

-Other veterans’ benefits (use code 127)

-Tax‑exempt First Nations pension income (use code 146)

-RCA payments (use T4A‑RCA)

-EBP payments (use T4)

8. Box 018 – Lump‑Sum Payments

Report taxable lump‑sum payments from:

RPPs

DPSPs

Unregistered pension plans

ALDAs

Over‑contribution reimbursements

Lump‑sum death benefits

Non‑resident service pension payments

DPSP allocations or reallocations

Do not report:

Direct transfers to RRSP/RRIF/RPP/PRPP (use Form T2151)

Tax‑exempt First Nations lump‑sums (use code 148)

9. Box 020 – Self‑Employed Commissions

Report commissions paid to independent agents.

Do not include GST/HST or PST.

10. Box 022 – Income Tax Deducted

Report only if you actually withheld tax.

Do not report:

-Garnishment amounts

-Requirement‑to‑pay amounts for past tax arrears

11. Box 024 – Annuities

Report annuity payments from:

RRSP refunds of premiums

LIFs and RRIFs

ALDAs

IAACs

DPSPs (annuity or instalments)

Do not report:

Pension/superannuation annuities (use Box 016)

VPLA payments (use code 133)

Life insurance policy annuities (use T5)

Payments to non‑residents (use NR4)

12. Box 048 – Fees for Services

Report fees paid for services other than employment.

Do not include:

-GST/HST or PST

-Payments that belong in Box 020 (commissions)

Special rule (2025+):

The trucking industry must report fees paid to CCPCs over $500.

13. Box 061 – Payer’s Program Account Number

Enter your 15‑character payroll account number on CRA copies only.

Do not include it on the recipient’s copy.

14. Other Information Codes (014–210)

The T4A has many additional codes. Students should understand the most common categories:

Income Types

028 — Other income

030 — Patronage allocations

040 — RESP accumulated income

042 — RESP educational assistance

046 — Charitable donations

104 — Research grants

105 — Scholarships, bursaries, fellowships

106 — Death benefits

107 — Wage‑loss replacement plan payments

117 — Loan benefits

118 — Medical premium benefits

119 — Group term life insurance premiums

Pension & Retirement‑Related

032 — RPP past service contributions

034 — Pension adjustment (MEP only)

036 — Plan registration number

037 — ALDA purchase

109 — Periodic payments from unregistered plans

110 — Pre‑1971 lump‑sum payments

115 — DPSP annuity payments

133 — Variable pension benefits

190 — Lump‑sum from unregistered plans

First Nations Exempt Income

144 — Other exempt income

146 — Exempt pension/superannuation

148 — Exempt lump‑sum payments

195 — Exempt PRPP payments

Education & Grants

130 — Apprenticeship grants

131 — RDSP payments

196 — Adult basic education tuition assistance

210 — Postdoctoral fellowship income

COVID‑19 Related

200 — COVID‑19 assistance

201 — Repayment of COVID‑19 assistance

15. Common Errors to Avoid

Reporting employment income on a T4A instead of a T4

Using Box 016 incorrectly for non‑annuity disability benefits

Forgetting Box 015 when Box 016 is filled

Reporting GST/HST in commission or fee amounts

Reporting direct transfers as income

Using the wrong code for First Nations exempt income

Reporting tax withheld when none was deducted

16. Key Takeaways

T4A slips cover a wide range of non‑employment income

Always match the payment type to the correct box or code

Dental benefit reporting applies only when pension/superannuation is reported

Many codes exist — accuracy depends on understanding the category

Consistency and documentation protect both payer and recipient

Program: Start Your Personal Tax (T1) Preparation Business

Module-3- Understanding Various T-Slips

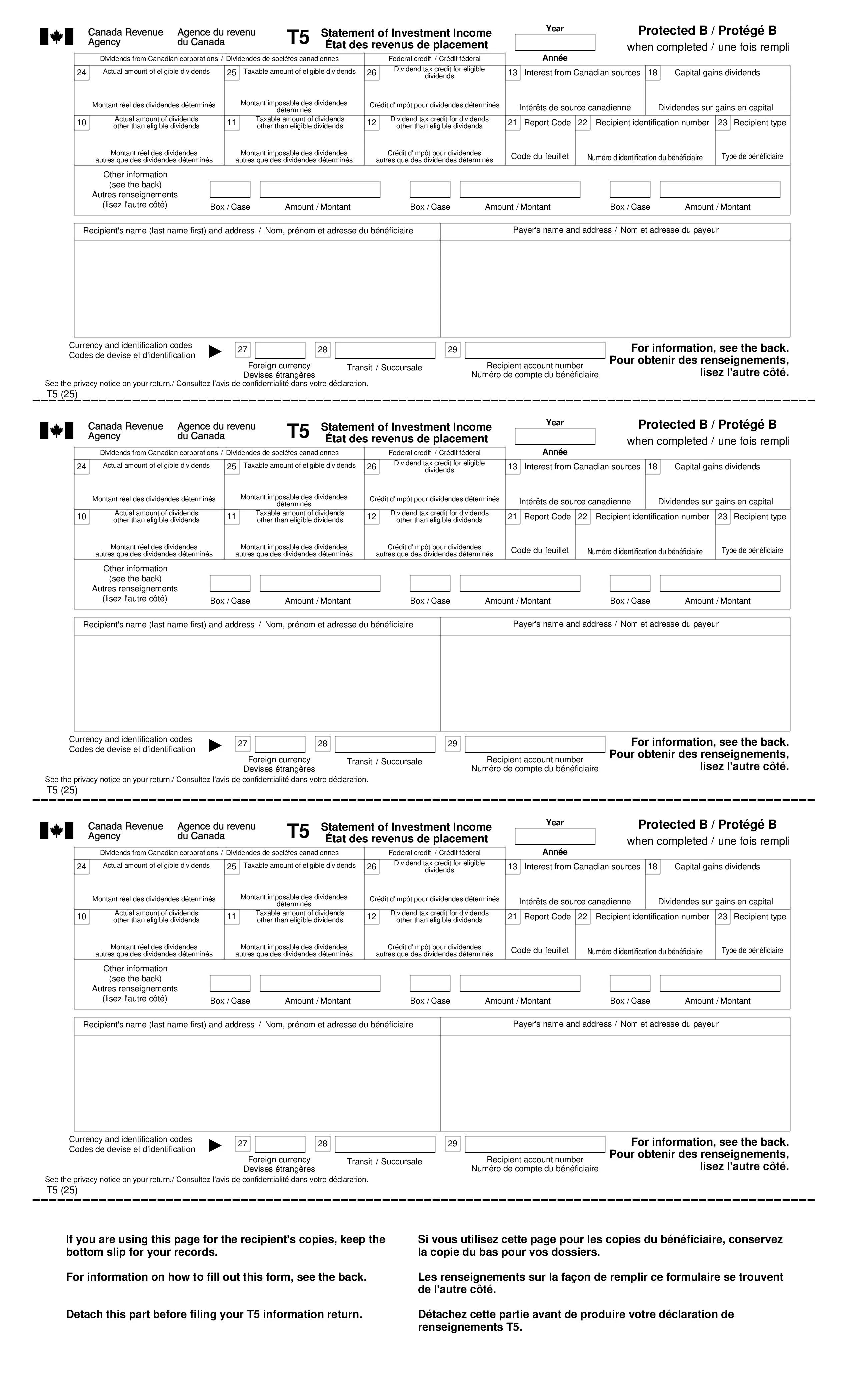

Lesson-M-3-L-3-T5-Investment Income (Interest and Dividends)

The T5 slip is used to report investment income paid to individuals, corporations, trusts, and other entities. These notes summarize the essential rules every bookkeeper, payroll preparer, and firm owner must understand when preparing T5 slips.

1. Purpose of the T5 Slip

A T5 slip reports investment income such as:

-Interest

-Dividends

-Capital gains dividends

-Royalties

-Certain annuity income

-Foreign income and foreign tax paid

It is used when the payer must report income from Canadian or foreign investment sources.

2. Recipient Name & Address

General Rules

Enter information in the white area provided.

If multiple recipients are entitled to the income (e.g., joint account), only one T5 slip is required.

Enter both names if two individuals share the income.

For corporations, trusts, associations, or institutions → enter the entity name, not an individual’s name.

Joint Accounts

Prepare one slip for the group. Include:

Primary representative’s name

Secondary representative (if known)

Primary representative’s SIN in Box 22

Code 2 in Box 23 to indicate a joint account

Special Recipient Types

Payments to a trust → use the trust name, not beneficiaries.

Payments to a registered holder (e.g., RRSP trustee) → use the registered holder’s name.

Formatting

First line: Last name → First name → Initials

Second line: Second recipient (if applicable)

Next lines: Full mailing address (city, province, postal code)

3. Payer Name & Address

Enter the payer’s full legal name and address on every T5 slip.

4. Year

Enter the calendar year in which the investment income was earned.

5. Dividends from Canadian Corporations

Dividends may be:

-Eligible dividends

-Other than eligible dividends

Dividends retain their character even when passed through another corporation.

Boxes 10, 11, 12 — Dividends Other Than Eligible Dividends

Box 10: Actual amount of dividends (non‑eligible)

Box 11: Taxable amount (actual + 15% gross‑up)

Box 12: Dividend tax credit (9/13 of gross‑up)

Do not include:

Credit union dividends (treated as interest)

Eligible dividends

Capital gains dividends

MIC dividends (reported in Box 13)

Boxes 24, 25, 26 — Eligible Dividends

Box 24: Actual amount of eligible dividends

Box 25: Taxable amount (actual + 38% gross‑up)

Box 26: Dividend tax credit (15.0198% of Box 25)

6. Box 13 – Interest from Canadian Sources

Report interest from:

Registered bonds/debentures

Money loaned or deposited with corporations, institutions, partnerships, trusts

Investment dealer accounts

Insurance policy interest

Expropriation compensation

Blended payments (interest portion)

Credit union dividends (non‑listed shares)

MIC taxable dividends (non‑capital gains)

Do not include:

Foreign interest (Box 15)

Interest paid by individuals (private mortgages)

Bank loan interest

Accrued annuity income (Box 19)

7. Other Information Area (Boxes 14–30)

This section contains blank boxes where you enter codes and amounts. If more than 3 codes apply → issue an additional T5 slip.

Box 14 – Other Income from Canadian Sources

Includes:

Dividends from non‑taxable Canadian corporations

Life insurance policy income

Eligible funeral arrangement (EFA) refunds

Box 15 – Foreign Income

Report gross foreign income in Canadian dollars

Include foreign spin‑off shares

Box 16 – Foreign Tax Paid

Report foreign tax withheld

Used by the recipient to claim foreign tax credits

Box 17 – Royalties

Payments for use of intellectual property or natural resources

Box 18 – Capital Gains Dividends

From:

Investment corporations

Mortgage investment corporations

Mutual fund corporations

Box 19 – Accrued Income: Annuities

Includes:

Accrued earnings on life insurance policies

Pre‑1990 annuity income

Box 21 – Report Code

Indicates slip status:

O – Original

A – Amended

C – Cancelled

Box 22 – Recipient Identification Number

SIN for individuals

Trust account number for trusts

Business number for corporations/partnerships

Box 23 – Recipient Type

Codes:

1 — Individual

2 — Joint account

3 — Corporation

4 — Association, trust, club, partnership

5 — Government or international organization

Box 27 – Foreign Currency

Use ISO currency codes (USD, EUR, GBP, etc.)

Only one currency per slip

If left blank → CRA treats amounts as CAD

Box 28 – Transit Code

Used by financial institutions.

Box 29 – Recipient Account Number

Optional account or policy number.

Box 30 – Equity‑Linked Notes Interest

Report deemed interest from linked notes under subsection 20(14.2).

8. Key Takeaways

T5 slips report investment income, not employment income.

Joint accounts require special handling (Box 22 + Box 23).

Dividends must be classified correctly as eligible or other than eligible.

Foreign income and foreign tax must be reported separately.

The “Other information” area contains many specialized codes — accuracy matters.

Always use the correct recipient type and identification number.